Semiconductor Fab Construction Economics and Timelines in 2026: Supply Chain Impacts

Table of Contents

- The 2026 Fab Construction Reality: Timelines vs. Promises

- The True 36-to-60 Month Timeline

- Economics of Capacity: Why Mature Nodes are Deprioritized

- Strategic Procurement Interventions

- 1. Dual Sourcing is Mandatory, Not Optional

- 2. Independent Distribution as a Bridge

- Frequently Asked Questions (FAQ)

- References

⚡ Sourcing Summary

Semiconductor fab construction requires high capital investment and a typical 36-month timeline. Delays are primarily driven by cleanroom qualification and fab tool lead times. Supply chain managers must maintain strategic buffers during construction.

Bottom Line Up Front (BLUF): While global semiconductor fabrication plant (fab) construction has accelerated in 2026 driven by the US CHIPS Act and European reshoring initiatives, the reality of deploying a high-yield operational cleanroom still spans 36 to 60 months. The capital expenditure (CAPEX) for a mature-node (28nm-65nm) fab now averages $4.5 billion due to localized labor constraints and material inflation. For procurement teams waiting for new capacity to alleviate shortages in industrial MCUs (like the NXP LPC1768FBD100) or legacy PMICs, relying on promised factory capacity is a critical supply chain risk. Proactive procurement must leverage independent distribution and strategic Last Time Buys (LTB) to bridge the 2026-2028 capacity gap.

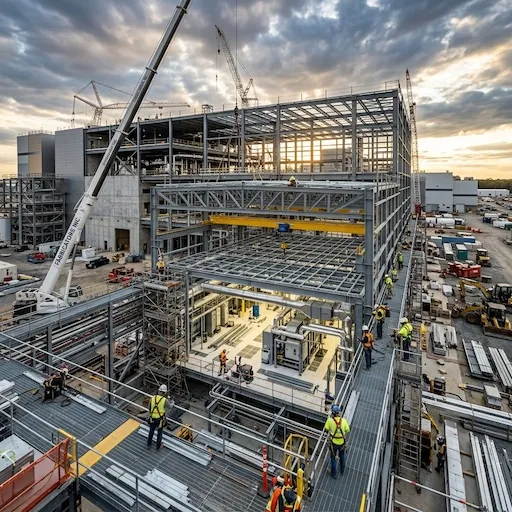

The 2026 Fab Construction Reality: Timelines vs. Promises

The announcement of a new semiconductor fab often triggers optimism across the supply chain. However, purchasing managers and engineering teams must differentiate between a “groundbreaking ceremony” and “commercial wafer output.” Building a semiconductor fabrication facility in 2026 is one of the most complex engineering endeavors on the planet.

The True 36-to-60 Month Timeline

Despite expedited permitting in certain jurisdictions, the fundamental physics and logistics of fab construction remain fixed.

- Facility Construction (Months 1-18): Pouring massive concrete sub-fab foundations designed to absorb microscopic seismic vibrations. Installing the labyrinth of chemical handling, ultra-pure water (UPW), and HVAC systems.

- Cleanroom Outfitting (Months 19-30): Achieving ISO Class 1 to Class 3 cleanroom standards. Delaying this phase due to shortages in specialized fluoropolymer piping or HEPA filters has been a common bottleneck in 2026.

- Equipment Move-in and Calibration (Months 31-42): The installation of lithography scanners, deposition chambers, and metrology tools. Lead times for trailing-edge semiconductor manufacturing equipment remain elevated at 14 to 18 months.

- Yield Ramp-up (Months 43-60+): Running test wafers, calibrating recipes, and achieving the 90%+ commercial yield required for profitability. This phase cannot be accelerated by capital alone.

Economics of Capacity: Why Mature Nodes are Deprioritized

The economics of a new fab heavily skew toward advanced nodes (3nm, 5nm) driven by AI and data center demand. For industrial and automotive OEMs relying on mature architectures (28nm, 45nm, 65nm), the math is unforgiving.

| Metrics (2026 Averages) | Advanced Node Fab (e.g., 3nm) | Mature Node Fab (e.g., 45nm/65nm) |

|---|---|---|

| Total CAPEX | $18B - $25B | $3B - $4.5B |

| Equipment Cost Share | ~80% (Extreme EUV reliance) | ~60% (DUV and legacy tooling) |

| Margin Profile | High (Premium pricing for AI/Logic) | Low to Moderate (Commoditized) |

| Incentive Funding Priority | High (National security focus) | Low (Except for specific automotive lines) |

Because the Return on Investment (ROI) for a mature node fab requires decades of high-utilization output, fewer foundries are breaking ground on new 65nm facilities. Instead, they are attempting to squeeze more efficiency out of fully depreciated 20-year-old lines. When legacy components like the Texas Instruments TPS51200DRCR DDR termination regulator experience demand spikes, there is no new fab capacity coming online to absorb the shock.

Strategic Procurement Interventions

Relying on future fab capacity to resolve current allocation issues is a dangerous procurement strategy. OEMs must take immediate defensive postures.

1. Dual Sourcing is Mandatory, Not Optional

If your BOM relies on a single-source proprietary MCU, the time to qualify a second source is now. For example, qualifying an alternative Cortex-M4 MCU requires software abstraction layers and rigorous hardware re-validation, a process that can take 12 months. Do not wait for an allocation notice to start.

2. Independent Distribution as a Bridge

When franchised distribution lines quote 52-week lead times for critical transceivers or power management ICs, independent distributors act as the strategic bridge. By tapping into global excess inventory pools from Tier-1 OEMs and EMS providers, independent distribution provides the necessary runway while long-term foundry capacity normalizes.

Note: Sourcing from the open market requires stringent quality assurance. Partner only with distributors utilizing ISO 17025 accredited third-party laboratories for decapsulation, X-ray inspection, and solderability testing.

Frequently Asked Questions (FAQ)

How long does it realistically take to build a new semiconductor fab in 2026?

Are new fabs being built for legacy and mature node chips (e.g., 65nm)?

How should procurement teams handle long lead times while waiting for new capacity?

References

- Global Semiconductor Fabrication Plant Expansion Report Q1 2026, SEMI.org, Accessed May 10, 2026. https://www.semi.org/

- The Economics of Mature Node Semiconductor Manufacturing, EE Times, Accessed May 12, 2026. https://www.eetimes.com/

SupplyICs Sourcing Team

Contact Our TeamIndependent Component Specialists

A team of veteran buyers navigating the global spot market. We specialize in locating hard-to-find, shortage, and EOL components. From strict anti-counterfeit verification to cross-reference matching, we provide frontline data to help you secure authentic stock safely.